The Evolution: From Banking to Finance

Open banking unlocked payment account data through APIs and consent frameworks. Financial institutions were mandated to grant third-party providers access to customer account information with explicit permission.

Open finance expands this principle beyond banking. It encompasses savings, investments, pensions, insurance, and mortgages the entire financial ecosystem. Instead of accessing single payment accounts, third parties can access comprehensive financial profiles with customer permission.

The Scope Shift:

• Open Banking: Limited to transactional banking data and payment accounts

• Open Finance: Encompasses entire financial ecosystem including investments, insurance, pensions, mortgages

• Result: From fragmented data access to comprehensive financial profiles enabling hyper-personalisation

Takeaway: Open finance extends open banking principles across all financial services, enabling third parties to access complete financial pictures with customer consent.

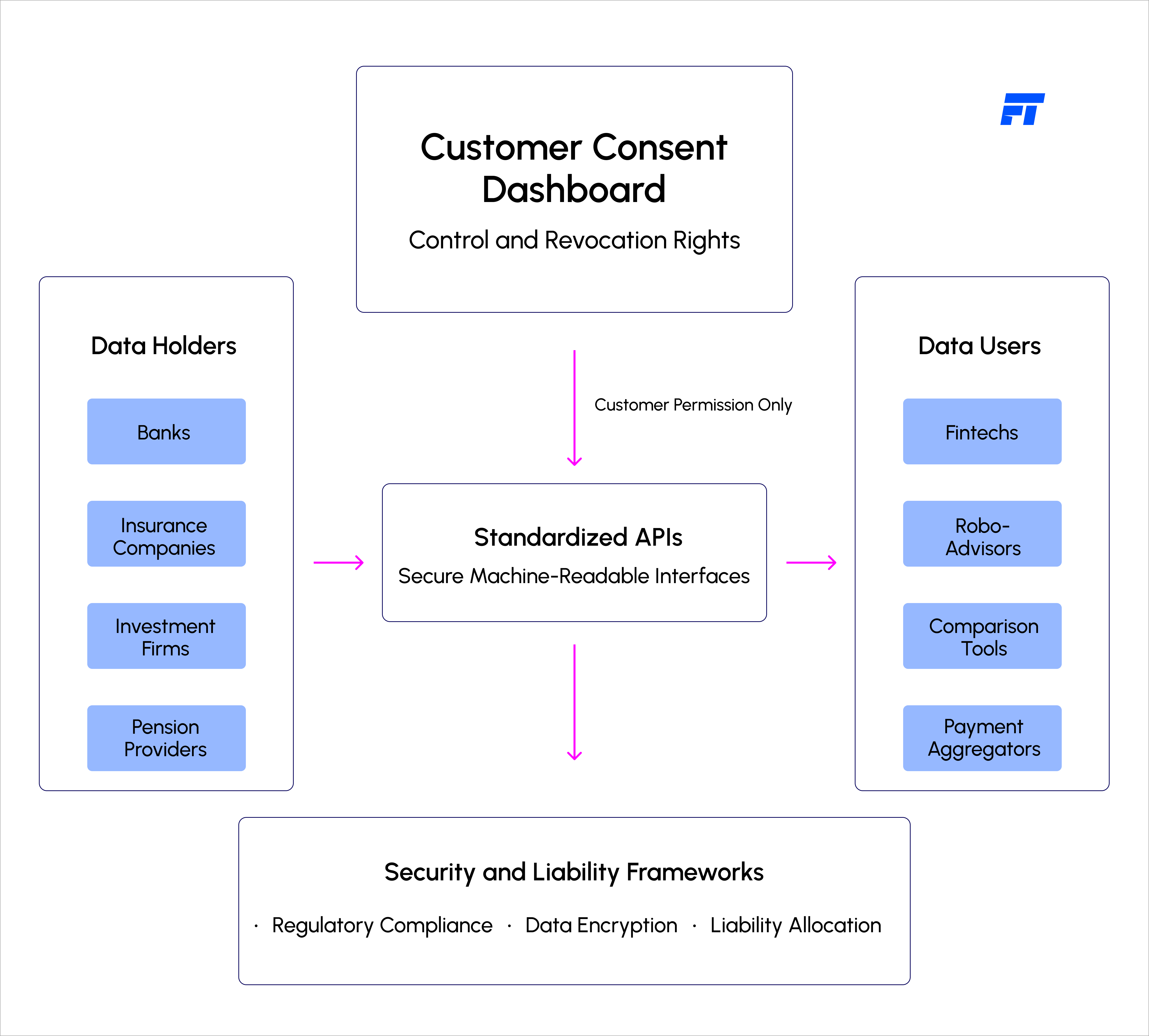

How Consent and Data-Sharing Frameworks Work

Consent is the foundation of both open banking and open finance. Customers grant explicit permission through digital dashboards, specifying which data can be shared, with whom, and for what purpose.

Data holders (banks, insurers, investment firms) are obligated to make data available through standardised technical interfaces. Data users (fintechs, advisors, comparison tools) access this data to create personalised products and services.

Framework Components:

• Consumer Consent: Explicit permission through dashboard, specifying duration and scope of data access

• Technical Standards: Standardised APIs enabling secure, machine-readable data transfer between systems

• Data Minimisation: Sharing only necessary data, protecting sensitive information through role-based access controls

• Liability Framework: Clear responsibility assignment for data breaches, with dispute resolution mechanisms

• Revocation Rights: Customers can withdraw consent anytime, stopping further data sharing immediately

Takeaway: Effective open finance requires consent dashboards, standardised APIs, clear liability frameworks, and customer revocation rights not technology alone.

Regional Approaches: Regulatory vs. Market-Driven

Regions are adopting fundamentally different governance models for open banking and open finance. Some mandate participation through regulation. Others encourage voluntary adoption, allowing market forces to drive innovation.

Understanding regional approaches is critical for financial institutions operating across geographies.

Governance Models:

• Regulation-Led (Europe, UK, Australia, Canada): Governments mandate data access, set standards, enforce compliance through central banks and financial regulators

• Market-Driven (US, Singapore, MENA): Institutions voluntarily cooperate on data sharing; government provides guidance but does not mandate participation

• Hybrid Approaches (APAC, LATAM): Mix of government mandates in major markets and industry-driven initiatives in developing markets

• Phased Implementation: Brazil implements in phases; Mexico developing frameworks; Indonesia prioritising financial inclusion

Takeaway: Regional fragmentation means no single global standard institutions must navigate multiple compliance frameworks simultaneously.

Key Regional Implementations: Open Banking & Open Finance

Open banking is evolving unevenly across regions. Regulatory intent, adoption speed, and scope vary widely, shaped by local market maturity and policy priorities.

- Europe & UK: PSD2-led open banking has reached 10–11% consumer adoption (2022), with regulators now expanding toward full open finance across savings, investments, and insurance.

- Australia: The Consumer Data Right (CDR) mandates data sharing across banking, energy, and telecom, making Australia one of the most comprehensive, compulsory data-sharing regimes globally.

- United States: A non-mandated, market-driven model relies on voluntary bank–fintech data sharing, resulting in slower adoption by incumbents despite fewer regulatory constraints.

- APAC (ex-Australia): Adoption is policy-encouraged but not mandated, with countries prioritising financial inclusion, leading to high regulatory fragmentation.

- LATAM: Brazil leads with a phased regulatory rollout, while others remain regulator-supported but market-driven, focused mainly on payments and lending.

- MENA: Central bank–mandated open banking in Saudi Arabia and Bahrain contrasts with the UAE’s collaborative model, reflecting a region-wide focus on controlled innovation and risk management.

Institutions operating across markets must design modular, compliance-by-design architectures that can adapt to fragmented regulatory realities while remaining future-ready for open finance expansion.

From APIs to Embedded Services

The visible impact of open finance shows up as embedded, contextual services instead of standalone banking apps.

Examples in 2026:

- E‑commerce: Buy Now, Pay Later and instant credit offers at checkout

- Wealth: Robo-advisors using full financial data, not just one account

- Insurance: Real-time quotes embedded in car, travel, or health journeys

- Payroll: Salary-linked loans, savings, and investments in HR platforms

- Aggregation: Single dashboards across banks, brokers, insurers, and pensions

Takeaway: Open finance turns financial services into components that plug directly into customer journeys.

What Banks and Fintechs Need to Get Right

Winning in an open finance world means building once and adapting to each region’s rules, rather than rebuilding for every market.

Execution Priorities:

- API-first architecture that can support multiple standards

- Centralised consent and preference management across products and regions

- Strong compliance and legal frameworks for data use and liability

- Real-time data integration from legacy cores into modern platforms

- Clear governance between product, tech, risk, and legal teams

Takeaway: The leaders will be the ones that treat open finance as infrastructure standardised, reusable, and compliant rather than as one-off projects.

Ready to navigate open finance implementation across regions?